Financial summons are legal notices requiring immediate attention to avoid further financial complications. Generally, such documents indicate a lawsuit filed by a creditor in relation to outstanding debts that they seek repayment for. A financial summons can have severe consequences such as judgments, wage garnishments, and liens on personal assets if ignored. Such considerations highlight the importance of taking prompt and informed action.

Dealing with a summons for debts from the courts is stressful and overwhelming in itself. Texas has many unique protections for debtors designed to safeguard certain assets, like homes and personal property. For example, the homestead exemption in the state protects primary residences, while most debts have limits on wage garnishment.

The Texas Office of Consumer Credit Commissioner highlights the prevalence of civil lawsuits related to debt, underscoring how common these challenges have become. Fortunately, Texas stands out for its strong debtor protections, providing residents with crucial financial relief. When dealing with being sued for debt in texas, you would respond quickly and understand your legal rights to better help guide you through the process successfully to protect your future.

A summons provides critical information, including the court date, the creditor’s name, and the amount claimed. Reviewing these details helps you prepare a response and understand the scope of the case. Ensure you note deadlines and legal requirements to avoid default judgments.

Errors can be made when filing debt lawsuits, such as miscalculations or incorrect information. Verify the debt owed, including the amount due, the identity of the creditor, and if it has passed the statute of limitations. If you're facing issues related to debt lawsuits or financial summons, it's crucial to better understand bankruptcy attorney in Worcester to guide you through the process and ensure accurate documentation and legal advice. This verification is critical in ensuring an accurate defense or negotiating more favorable terms.

Failure to respond will automatically result in a judgment against you, and creditors can intensify their collection efforts. File an official response with the court within the time frame allowed to protect your rights. Doing so also enables you to object to errors and even settle the case.

Professional legal representation will clarify the details of your case and assist in creating a powerful defense. Texas non-profit groups provide free or low-cost legal services for debt-related lawsuits against debtors. Lawyer representation can sometimes mean settlement decreases or dismissal.

Texas law affords great protections for debtors. No creditor can take your homestead, meaning you and your family will have a place to live no matter what. Other exemptions protect tools of trade, retirement accounts, and some personal property.

Texas wage garnishments exist under specific debts, such as those against child support or unpaid taxes giving most residents financial security over others. Adding this advantage together with a four-year statute of limitations against filing collection lawsuits in the state of Texas positions it as one of the country's debtor-friendly states. An empowered individual is equipped with what will help him or her in challenging those legal disputes.

Understanding the difference between financial summons and collection notices is very important. A financial summons is a legal paper indicating that a creditor has filed a lawsuit, requiring a court appearance or formal response. Collection notices, on the other hand, are informal communications from creditors to settle outstanding debts without the use of legal proceedings.

A collection notice is a warning, but a financial summons demands action. If a summons is not responded to, it can lead to serious legal and financial repercussions, so it is imperative to respond promptly and appropriately.

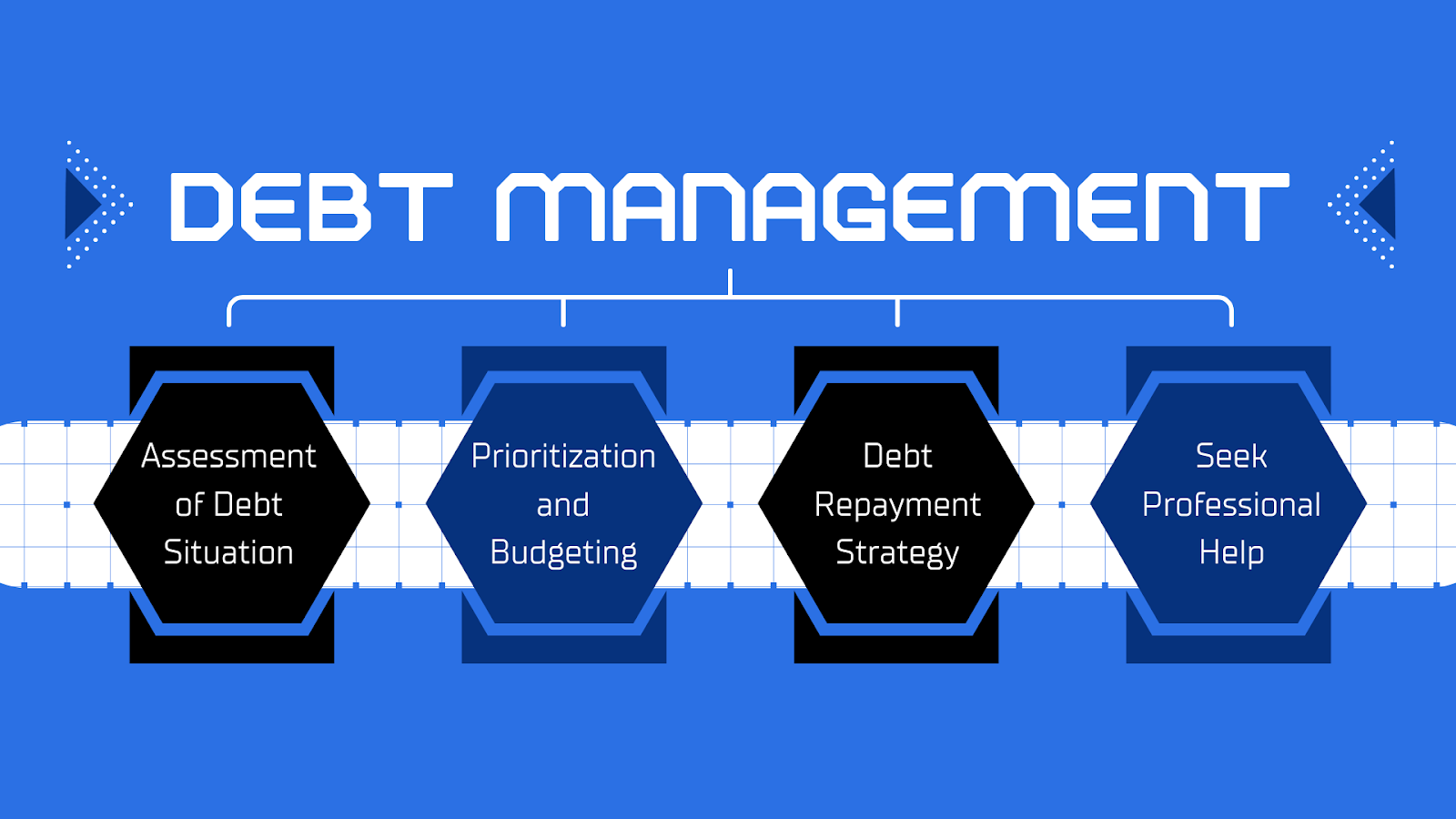

Paying in a lump sum can encourage creditors to accept lesser amounts than what is due. This is most effective when you have liquid assets available and want to resolve the issue as soon as possible.

If you are unable to pay in one lump sum, then negotiate an affordable repayment plan with your creditor. Ensure that you have any agreement in writing to avoid later disputes and to protect your rights.

Professionals who specialize in debt negotiation can also be intermediaries for you in obtaining better settlement terms. These experts are very useful, especially when dealing with aggressive creditors or large debts.

Negotiation in advance prevents the lawsuit from getting worse. You save time, stress, and financial strain.

The best way to avoid future financial summons is to proactively manage finances. Budgeting allows you to monitor all your expenses and thus can guide you on which you must repay first. An emergency fund helps cushion the shocks in unexpected financial challenges.

Another way to avoid the lawsuits is to maintain open communication with creditors. Many creditors are willing to work with individuals who put in good faith efforts to repay the debts. Early resolution of financial difficulties reduces the potential for legal action and helps you stay in control of your financial health.

Some resources exist for Texans fighting back against lawsuits over debt: The legal aid organizations provide advice absolutely free or at reasonable fees to those having financial difficulties, and some non-profit agencies that work as credit counseling agencies with advice on making a budget and consolidating debt.

Educational programs focusing on financial literacy empower individuals to make informed decisions and avoid future legal issues. Leveraging these resources ensures that you have the tools and knowledge to handle financial summons effectively.

What should I do if I cannot afford to pay a debt in Texas?

Negotiate directly with the creditor or seek bankruptcy. Texas law protects essential assets, so you won't be left destitute at the end of the debt resolution process.

How long does a creditor have to sue for debt in Texas?

The statute of limitations for most debts in Texas is four years. After that time, creditors cannot file lawsuits but can still try to collect informally.

Will a financial summons impact my credit score?

Of course, a debt-related lawsuit definitely lowers the credit score significantly. Settling such a lawsuit quickly reduces long-term damage to the credit.

The financial summons requires prompt and intelligent action to minimize legal and financial consequences. Knowing your rights, tapping into debtor protections in Texas, and accessing professional advice will help you work through these problems successfully. In fact, proactively managing your debt and communicating with creditors may make it easier for you to ensure a solid financial future while avoiding undue stress.